Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

By Gregory Brock], California Real Estate Broker & Attorney | Bay Area

In the complex landscape of San Francisco Bay Area real estate, the distinction between an incorporated city and an unincorporated community is more than just a matter of address. It is a significant and often overlooked financial variable. People sometimes overlook the “tax arbitrage” available by selecting a home just across a municipal boundary. And people are sometimes surprised by hidden costs that attach to an unincorporated address that they did not anticipate.

In Alameda County and Contra Costa County, whether a property is “unincorporated” (governed directly by the County Board of Supervisors) or “incorporated” (within the limits of a city such as Oakland, Richmond, or Berkeley) has a direct, measurable impact on both the closing costs and the carrying costs of a residence. The differences are not trivial. On a $1.5 million home, the location of the property relative to a municipal boundary can mean a swing of more than $20,000 at the closing table alone.

This article explains those differences systematically, from the one-time transfer taxes paid at closing to the annual property tax bill, special assessments, permit requirements, and point-of-sale ordinances that vary by jurisdiction. This is for buyers and sellers who want to make fully informed decisions.

PART ONE: WHAT DOES “UNINCORPORATED” ACTUALLY MEAN?

California’s counties contain two types of territory: incorporated cities (which have their own city governments, city councils, and municipal service departments) and unincorporated areas (which are governed directly by the elected Board of Supervisors of the county). Unincorporated communities often carry familiar neighborhood names — Alamo, Blackhawk, Bay Point, Diablo, Kensington, and El Sobrante in Contra Costa County; Castro Valley, Cherryland, San Lorenzo, Ashland, Fairview, and Sunol in Alameda County — but they are legally not cities. There is no mayor, no city council, and no city police department.

This matters for real estate transactions in several ways. Incorporated cities may levy their own documentary transfer taxes in addition to the county tax. They enact their own building codes and permit fee schedules. They pass their own voter-approved bonds and parcel taxes. And some cities have adopted local point-of-sale ordinances that require inspections, certifications, or physical improvements as a condition of transferring title. In an unincorporated area, none of those city-level impositions apply — the county’s rules govern instead.

This does not mean that unincorporated areas are categorically cheaper to buy, sell, or own property in. The county has its own layers of taxation and assessment, and certain unincorporated communities carry specialized charges — Geologic Hazard Abatement District (GHAD) assessments, Community Facilities District (Mello-Roos) special taxes, and private road and utility obligations — that can rival or exceed what a city homeowner pays. The analysis requires looking at the entire tax and fee picture, not just the presence or absence of a city transfer tax.

PART TWO: THE DOCUMENTARY TRANSFER TAX — THE BIGGEST TRANSACTION-COST VARIABLE

- The State Framework

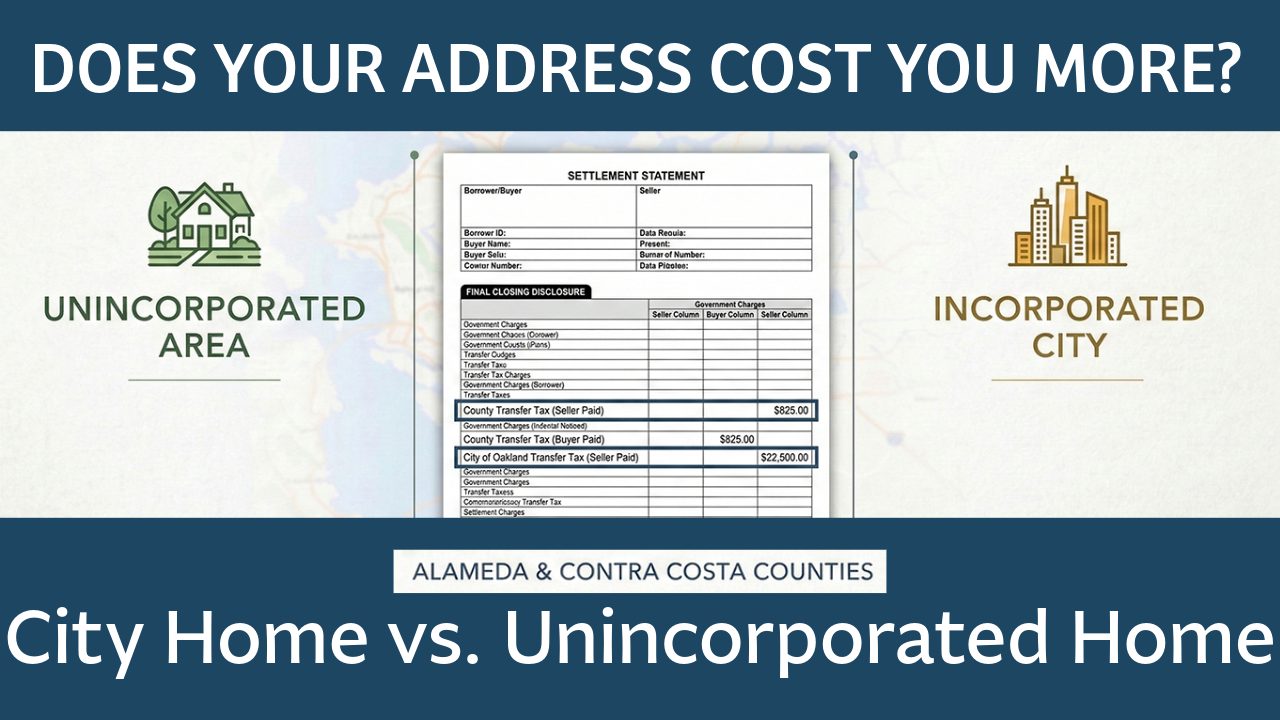

California’s Revenue and Taxation Code authorizes counties to impose a documentary transfer tax (DTT) on every deed that records a transfer of real property. The statewide county rate is uniform: $1.10 per $1,000 of value. The value is rounded up to the nearest $500 before the calculation is applied. This county DTT applies throughout both Contra Costa and Alameda Counties, whether the property is inside a city or in an unincorporated area.

Cities have separate authority under California law to impose their own city-level documentary transfer tax, collected in addition to the county tax. Cities that exercise this authority are sometimes referred to as “Charter Cities” — though technically, cities may also impose transfer taxes under the Revenue and Taxation Code. The important practical point is that when a city imposes its own transfer tax, it is layered on top of the county’s tax, not in lieu of it. The result is that a home inside certain cities carries a dramatically higher transfer tax burden than an identical home sold the same day just outside city limits in an unincorporated area.

For unincorporated areas, no city-level tax applies. The county-only rate of $1.10 per $1,000 is all that is due.

- Contra Costa County: Transfer Tax Rates by Jurisdiction

Contra Costa County collects $1.10 per $1,000 of value on all transfers countywide. For a home sold at roughly $800,000, the county DTT is approximately $880. That amount applies whether the home is in Walnut Creek, Danville, Concord, or in the unincorporated communities of Alamo, Blackhawk, or Bay Point.

Within Contra Costa County, only two cities currently impose a city-level transfer tax: Richmond and El Cerrito. All other cities in Contra Costa County — including Walnut Creek, Concord, Danville, Lafayette, Orinda, Moraga, Pleasant Hill, Martinez, Brentwood, Antioch, Pittsburg, and Hercules — impose no city transfer tax. This means that for most intra-county comparisons, the transfer tax cost is the same in an unincorporated area as it is in a city.

Richmond is the notable exception, and its transfer tax is not only the highest in Contra Costa County — it is one of the most steeply tiered in the Bay Area:

| Jurisdiction | City Transfer Tax Rate | Total Rate (City + County) | Tax on $800K Sale |

| Unincorporated CCC (all communities) | None | $1.10 / $1,000 | ~$880 |

| El Cerrito | $12.00 / $1,000 (flat) | $13.10 / $1,000 | ~$10,480 |

| Richmond (up to $1M) | $7.00 / $1,000 | $8.10 / $1,000 | ~$6,480 |

| Richmond ($1M–$3M) | 1.25% ($12.50 / $1,000) | $13.60 / $1,000 | ~$10,880 on $800K (N/A — below $1M) |

| Richmond ($3M–$9.99M) | 2.5% ($25.00 / $1,000) | $26.10 / $1,000 | ~$78,300 on $3M sale |

| Richmond ($10M+) | 3.0% ($30.00 / $1,000) | $31.10 / $1,000 | — Luxury tier |

| Walnut Creek, Concord, Danville, Lafayette, Orinda, Moraga, Pleasant Hill, Martinez, Brentwood, Antioch, Pittsburg, Hercules, Pinole, San Pablo | None | $1.10 / $1,000 | ~$880 |

* Richmond’s rate rounds the sales price up to the nearest $1,000 before calculating. Rates confirmed against Contra Costa County Recorder and Richmond municipal records. Always verify current rates before closing.

A critical correction to note: some published summaries have stated that San Pablo and Pinole impose city transfer taxes in Contra Costa County. Based on current county recorder records and the WFG Title transfer tax schedule, neither San Pablo nor Pinole imposes a city-level documentary transfer tax. Only Richmond and El Cerrito do so in Contra Costa County. Readers should verify with the county recorder’s office before closing, as ordinances can change.

- Alameda County: A Very Different Story

Alameda County presents a far more consequential picture. The county itself collects $1.10 per $1,000, paid by the buyer under Alameda County custom. However, nearly all of the county’s major cities impose their own substantial city-level transfer taxes on top of the county rate. Several of these rates are among the highest in the United States.

| City / Area | City Transfer Tax (tiered where noted) | Total w/ County | Tax on $900K Sale |

| Unincorporated Alameda County (Castro Valley, San Lorenzo, Cherryland, Ashland, Sunol, etc.) | None | $1.10 / $1,000 | ~$990 (buyer) |

| Oakland | Up to $300K: $10.00; $300K–$2M: $15.00; $2M–$5M: $17.50; $5M+: $25.00 (all per $1,000) | $16.10 / $1,000 (mid-tier) | ~$13,500 city tax + ~$990 county = ~$14,490 |

| Berkeley | Up to $1.7M: $15.00 / $1,000; Above $1.7M: $25.00 / $1,000 | $16.10 / $1,000 (under $1.7M) | ~$13,500 city + ~$990 county = ~$14,490 |

| Albany | $15.00 / $1,000 (flat) | $16.10 / $1,000 | ~$13,500 city + ~$990 county = ~$14,490 |

| Alameda (City) | $12.00 / $1,000 (flat) | $13.10 / $1,000 | ~$10,800 city + ~$990 county = ~$11,790 |

| Emeryville | Up to $1M: $12.00; $1M–$2M: $15.00; $2M+: $25.00 (per $1,000) | $13.10 / $1,000 (under $1M) | ~$10,800 city + ~$990 county = ~$11,790 |

| Piedmont | $13.00 / $1,000 (flat) | $14.10 / $1,000 | ~$11,700 city + ~$990 county = ~$12,690 |

| San Leandro | $11.00 / $1,000 (flat) | $12.10 / $1,000 | ~$9,900 city + ~$990 county = ~$10,890 |

| Hayward | $8.50 / $1,000 (flat) | $9.60 / $1,000 | ~$7,650 city + ~$990 county = ~$8,640 |

| Fremont, Dublin, Livermore, Newark, Pleasanton, Union City | None | $1.10 / $1,000 | ~$990 (county only) |

* Oakland’s rates are confirmed against current Oakland city ordinance (Measure X, effective January 1, 2019). Berkeley’s $1.6M threshold adjusts annually with a cost-of-living index. Emeryville is tiered at higher price points. All rates as of early 2025. Verify with Alameda County Recorder before closing.

The financial stakes in Alameda County are dramatic. A home sold for $900,000 in unincorporated Castro Valley generates a total documentary transfer tax of approximately $990, paid by the buyer under county custom. The same home sold in Oakland, Berkeley, or Albany carries a transfer tax burden of approximately $14,490 — a difference of more than $13,500 on a single transaction. For a $1.5 million home in Berkeley, the total transfer tax (city plus county) exceeds $24,000. An equivalent home in unincorporated territory generates roughly $1,650. This is a material transaction cost that can easily exceed a month’s mortgage payment, and it directly affects both the seller’s net proceeds and the buyer’s closing cost budget.

- Who Pays the Transfer Tax, and Is It Negotiable?

The allocation of transfer tax between buyer and seller varies by jurisdiction and local custom — and it is important to understand that the “custom” is not always what people assume.

In Contra Costa County and Alameda County, the county documentary transfer tax is traditionally paid by the seller. For city transfer taxes within Alameda County, the allocation varies by city: Oakland’s city transfer tax is split 50/50 between buyer and seller. Berkeley’s city transfer tax, by longstanding local custom, is traditionally paid entirely by the buyer. Other cities vary. These customs are embedded in how escrow instructions are typically drafted, and they materially affect who should be budgeting for what.

Critically, all California real estate closing costs are negotiable between the parties. Nothing prevents a buyer and seller from agreeing to shift, split, or absorb any of these taxes as part of the overall purchase negotiation. In higher-transfer-tax cities like Berkeley, it is not uncommon for buyers to attempt to negotiate seller contribution to the city transfer tax when market conditions allow. In all cases, both parties should understand the full tax burden before offer terms are finalized.

For unincorporated areas in either county, there is no city transfer tax to allocate. The only transfer tax is the county DTT, paid according to county custom (seller in Contra Costa; buyer in Alameda), plus the county’s share of the SB 2 recording fee. This simplifies the closing cost calculation considerably.

PART THREE: ONGOING PROPERTY TAXES — THE LAYERED QUESTION

- The Proposition 13 Foundation

All California real property is subject to Proposition 13 (1978), which caps the base property tax rate at 1% of assessed value — the purchase price for newly acquired property — with annual increases in assessed value limited to 2% per year or the rate of inflation, whichever is lower. This 1% base rate applies uniformly statewide, whether the property is inside a city or in unincorporated county territory. It is not what varies.

What varies — and what can push the effective tax rate from roughly 1.10% to as high as 1.50% or more in some areas — is the accumulating weight of voter-approved add-ons layered on top of the Prop 13 base.

- The Add-On Stack: What Gets Layered on Top of 1%?

General Obligation Bonds (Ad Valorem): When a school district, city, community college district, or other entity asks voters to approve a bond measure, the annual debt service (principal and interest) is allocated to property tax bills within that entity’s boundaries. A school district’s boundaries, for example, may include both incorporated city parcels and unincorporated county parcels — so school bond assessments are not strictly an incorporated-vs-unincorporated distinction. However, city-specific bonds (for city parks, libraries, city police facilities) apply only to parcels within the city.

Parcel Taxes: Unlike ad valorem assessments, parcel taxes are flat per-parcel charges and require a two-thirds supermajority vote to pass. They fund schools, libraries, fire districts, and other local services. Parcel taxes are especially prevalent in Berkeley, Oakland, and other urban Alameda County cities, where layers of successive voter-approved parcel taxes can add $500 to $1,500 or more annually to a homeowner’s bill. Unincorporated areas generally do not carry this layer of city-specific parcel taxes, though county-wide and school district parcel taxes apply to all parcels.

Mello-Roos / Community Facilities District (CFD) Special Taxes: Created by the Mello-Roos Community Facilities Act of 1982, CFD special taxes fund infrastructure and services in newly developed communities. They are not limited by Proposition 13 because they are levied as special taxes, not ad valorem assessments. Mello-Roos taxes can range from a few hundred to several thousand dollars annually and can persist for up to 40 years until the underlying bonds are retired. This is not exclusively an unincorporated phenomenon — CFDs exist within cities too — but many large new developments in unincorporated portions of both counties were required by the county to fund infrastructure through CFDs. Buyers in newly developed unincorporated communities in Contra Costa County (portions of Bay Point, Discovery Bay, Oakley) must scrutinize this carefully.

Direct Assessments / Special District Charges: Parcels in both incorporated and unincorporated areas may be subject to direct assessments for services managed by special districts: East Bay Municipal Utility District, East Bay Regional Park District, local fire protection districts, vector control districts, mosquito abatement districts, and others. In unincorporated areas, some services that a city would provide through its general fund (street lighting, landscaping, drainage) are instead funded through special assessment districts that appear as direct charges on the tax bill.

Geologic Hazard Abatement Districts (GHADs): GHADs are California-specific and are more concentrated in unincorporated hillside communities in both counties. A GHAD is formed to manage landslide risk, slope stabilization, erosion control, and related geologic hazard mitigation within a defined area. GHAD assessments fund ongoing monitoring and remediation. Communities like Blackhawk and portions of the unincorporated Contra Costa hillsides have GHAD assessments that appear as annual property tax charges. These are not typically present in incorporated flatlands cities.

- Practical Comparison of Effective Property Tax Rates

As a working estimate, buyers purchasing in unincorporated areas of either county should plan on an effective property tax rate of approximately 1.15% to 1.35% of purchase price for their first year. Buyers in Oakland should plan on approximately 1.35% to 1.50% or higher, driven by the extensive stack of city-specific bonds and parcel taxes. Berkeley is in a similar range to Oakland.

That said, these are generalizations. The effective rate for any specific parcel depends on its Tax Rate Area (TRA) code — a number assigned by the county that identifies every taxing entity with jurisdiction over that parcel. Both the Contra Costa County Assessor and the Alameda County Assessor maintain online parcel lookup tools that show the current TRA and the associated tax rate. Buyers should look up the specific TRA for any property they are considering, apply it to the purchase price, and add any known Mello-Roos or GHAD charges to arrive at a realistic first-year estimate.

The critical buyer mistake to avoid: do not use the seller’s current tax bill as a proxy for your future tax bill. A seller who purchased the property in 1994 may have an assessed value of $200,000 on a home now selling for $1.2 million. Your base property tax will be assessed on the purchase price, not the prior owner’s basis. The effective rate is applied to the purchase price, not to the seller’s historic assessed value.

PART FOUR: POINT-OF-SALE ORDINANCES — A HIDDEN COST IN INCORPORATED CITIES

Beyond transfer taxes and property taxes, incorporated cities — particularly in Alameda County — have adopted “point-of-sale” (POS) ordinances that impose mandatory inspections, certifications, or physical improvements as conditions of transferring title. These obligations add direct cost and potential transaction delay to sales within those cities. They are generally absent in unincorporated areas, where no city ordinance applies and county-level POS requirements are more limited.

- Oakland: Sewer Lateral and Sidewalk Compliance

Oakland requires both private sewer lateral (PSL) compliance and sidewalk compliance as conditions of transferring residential property. The private sewer lateral ordinance requires that the sewer line connecting the home to the city main be pressure-tested, inspected, and certified as leak-free. Repairs or replacement can cost anywhere from a few hundred to several thousand dollars, depending on the age and condition of the lateral. The responsibility for compliance — and who bears the cost — is negotiable between buyer and seller, but must be addressed.

The sidewalk ordinance (adopted July 2019) requires that the sidewalk adjacent to the property be inspected by a licensed contractor and, if deficient, repaired or replaced as a condition of title transfer. A Compliance Certificate must be obtained, or a Provisional Certificate can be issued for a 90-day period during which the work is completed. Permit fees apply. Corner lots with two sidewalk segments can face material sidewalk replacement costs.

- Berkeley: Sewer and BESO Energy Disclosure

Berkeley also requires private sewer lateral compliance at point of sale. In addition, Berkeley has adopted its Building Energy Saving Ordinance (BESO), which requires that residential properties be assessed for energy efficiency and that findings be disclosed to the buyer in an energy report. Importantly, BESO does not currently require the seller to make any energy efficiency improvements — it is a disclosure requirement, not a repair mandate. However, the assessment itself costs money (typically $200 to $400 for a single-family home), and the results are disclosed to prospective buyers, potentially affecting negotiations.

- Other Jurisdictions

Other Alameda County cities have their own variations. Some require water-conserving fixture retrofits. Some require seismic gas shutoff valves. Hayward and other cities may have their own sewer compliance requirements. The details change over time as ordinances are amended. Any seller in an incorporated Alameda County city should confirm current POS requirements with their agent and the applicable building department well before listing.

- The Unincorporated Advantage

In unincorporated areas of both Contra Costa and Alameda Counties, no equivalent city-level POS mandates apply. County-level health and safety requirements exist (particularly regarding septic systems in areas not served by public sewer), but the mandatory pre-sale inspection and compliance infrastructure that characterizes Oakland and Berkeley transactions does not. This means fewer third-party certifications to obtain, less potential for pre-closing repair obligations to generate disputes, and in general a smoother path to closing.

PART FIVE: PERMIT FEES, BUILDING JURISDICTION, AND REGULATORY DIFFERENCES

For buyers who plan to remodel, add an ADU, or make improvements after purchase, the identity of the permitting authority — city or county — has practical implications.

Within an incorporated city, permits are issued by the city’s building department, which sets its own fee schedule and may have adopted local amendments to the California Building Code that impose requirements beyond state minimums. Berkeley’s building department, for example, is known for detailed review processes and fees that can be higher than surrounding jurisdictions. Oakland’s permitting system has historically experienced processing backlogs that add time to projects.

In unincorporated areas, the Contra Costa County Building Inspection Division or the Alameda County Community Development Agency (CDA) has jurisdiction. County permit fee schedules and code interpretations differ from the individual cities. In some categories, county fees are lower than high-overhead city departments; in others they are comparable. What is clear is that the bureaucratic culture, staffing levels, and processing times differ, and buyers with immediate renovation plans should investigate the relevant permit office’s current performance before making assumptions about project timelines.

One specific advantage worth noting: Contra Costa County and Alameda County have in recent years adopted more permissive ADU (accessory dwelling unit) ordinances in their unincorporated territories, in some cases exceeding the flexibility offered by neighboring city ordinances. Buyers interested in adding rental income through an ADU should review the applicable county ADU rules for any unincorporated property under consideration. County zoning for unincorporated areas can sometimes offer more flexibility for certain uses than would apply within a city with stricter local zoning.

PART SIX: OTHER TRANSACTION-COST ITEMS — WHAT DOES NOT CHANGE

Several transaction costs are uniform across incorporated and unincorporated areas within the same county, and it is worth identifying them to avoid confusion:

County Recording Fees: The Contra Costa and Alameda County Recorders charge the same fees to record deeds regardless of whether the property is inside a city or in an unincorporated area. As of 2025, both counties are subject to the SB 2 Building Homes and Jobs Act fee ($225 per document, with certain exemptions for owner-occupied residential transactions). Recording fees are countywide and uniform.

Title Insurance: Title insurance premiums are calculated based on purchase price using rates filed by the insurer, not by the location of the property within a county. The unincorporated vs. incorporated distinction does not directly affect the title premium rate.

Escrow Fees: Escrow fees are negotiated between the parties and the escrow company and are based on the purchase price and complexity of the transaction, not on whether the property is inside a city.

What can differ is the complexity of title examination for certain unincorporated properties. Parcels in rural or semi-rural unincorporated areas may have complex easement histories, private road maintenance agreements, or water company interests that require more underwriting attention. These issues may result in title exceptions or endorsements that add cost. Buyers of unincorporated properties — particularly those served by private roads or private utility infrastructure — should review the preliminary title report carefully.

PART SEVEN: FIRE INSURANCE AND THE WILDLAND-URBAN INTERFACE

This is not a transfer tax or a closing cost in the traditional sense, but it has become a material and rapidly changing ownership cost that distinguishes certain unincorporated properties from their urban city counterparts, and it must be addressed in any honest comparison.

Unincorporated hillside and semi-rural communities in both Contra Costa and Alameda Counties are disproportionately located in territory designated as High or Very High Fire Hazard Severity Zones (FHSZ) by Cal Fire. Properties in these zones face restricted availability of standard homeowners insurance, higher premiums, and in some cases can only be insured through the California FAIR Plan — the insurer of last resort, which provides less comprehensive coverage at higher cost than a standard policy. The FAIR Plan situation in California has deteriorated significantly in recent years as major insurers have exited or limited their California exposure.

Cal Fire’s FHSZ designation is a required disclosure on the Natural Hazard Disclosure Statement. Buyers of any unincorporated property in a hillside or wildland-adjacent area of either county should obtain insurance quotes from multiple carriers before removing contingencies. A $1,400 annual homeowners insurance premium for a comparable home in an Alameda County flatlands city could easily become $4,000 to $8,000 or more annually for an unincorporated hillside home with limited insurer options — or be limited to FAIR Plan coverage with gaps that require supplemental fire protection policies.

This cost differential is one of the few areas where an unincorporated address may carry a material annual cost premium compared to an urban city address in the same county.

PART EIGHT: SIDE-BY-SIDE COMPARISON — THE NUMBERS IN CONTEXT

To consolidate the foregoing into a usable reference, the following table compares four scenarios: (1) unincorporated Castro Valley, Alameda County; (2) Oakland; (3) unincorporated Alamo, Contra Costa County; and (4) Berkeley. All scenarios assume a $900,000 purchase price.

| Cost / Factor | Uninc. Castro Valley (Alameda Co.) | City of Oakland (Alameda Co.) | Uninc. Alamo (Contra Costa Co.) | City of Berkeley (Alameda Co.) |

| County DTT | ~$990 (buyer) | ~$990 (buyer) | ~$880 (seller) | ~$990 (buyer) |

| City DTT | None | ~$13,500 (50/50 split) | None | ~$13,500 (buyer by custom) |

| Total Transfer Tax | ~$990 | ~$14,490 | ~$880 | ~$14,490 |

| Est. Effective Property Tax Rate (Year 1) | ~1.15–1.30% | ~1.35–1.50% | ~1.15–1.35% | ~1.35–1.50% |

| Annual Tax on $900K Assessed Value | ~$10,350–$11,700 | ~$12,150–$13,500 | ~$10,350–$12,150 | ~$12,150–$13,500 |

| Potential Mello-Roos / CFD Tax | Possible ($0–$2,000/yr) | Possible ($0–$1,000/yr) | Possible (esp. newer devs.) | Less common (older city) |

| GHAD Assessment (hillside) | Possible in hills areas | Uncommon | Yes in parts of Alamo / Blackhawk | Uncommon |

| Point-of-Sale Ordinances | None (county only) | Yes: sewer + sidewalk | None (county only) | Yes: sewer + BESO energy report |

| Permit Jurisdiction | Alameda County CDA | City of Oakland | CCC Building Inspection | City of Berkeley |

| Fire Insurance Risk Premium | Moderate (low-lying areas) to High (hills) | Moderate (urban) | Moderate to High (esp. hillside) | Moderate (urban) |

| HOA Fees (if applicable) | Generally none | Possible (condos/planned) | Common in Alamo, Blackhawk | Possible (condos) |

All figures are estimates for illustration purposes. Actual costs depend on the specific parcel, current TRA code, active bonds, and market conditions. Consult your escrow company and a qualified tax advisor before closing.

PART NINE: PROS AND CONS — THE COMPLETE PICTURE

From a purely fiscal standpoint, buying or selling in an unincorporated area is almost always cheaper at the point of sale due to the absence of a city transfer tax. But the analysis does not end there. The following is an honest summary of the tradeoffs:

| Advantages of Unincorporated Areas | Advantages of Incorporated Cities |

| No city transfer tax — significant savings at closing (can exceed $20,000 in Alameda County) | Direct access to city police department (vs. county sheriff) |

| Generally fewer city-wide parcel taxes and city bond assessments on the annual tax bill | City council representation and more localized political accountability for land use decisions |

| No city point-of-sale ordinances (no mandatory sewer/sidewalk/BESO inspections at closing) | Stricter local zoning and design review can preserve neighborhood character and property values |

| Potentially more flexible zoning and ADU rules under county ordinance in some areas | Easier access to city programs: neighborhood services, city parks, city library systems, business licensing |

| County building departments may have different (sometimes more straightforward) fee structures for permits | In Alameda County, buyers in cities like Fremont, Dublin, or Pleasanton pay no city transfer tax — same outcome as unincorporated territory |

| Potential disadvantages: GHAD assessments (hillsides), fire insurance cost (FHSZ areas), HOA fees in master-planned communities, Mello-Roos in newer developments | Potential disadvantages: high transfer tax in Oakland/Berkeley/Albany/Alameda; higher effective property tax rate from accumulated parcel taxes and bonds; POS compliance costs at time of sale |

PART TEN: PRACTICAL STEPS FOR BUYERS AND SELLERS

For Sellers

- Before listing, confirm the exact jurisdiction of your property. Use the County Assessor’s parcel lookup tool. A surprising number of sellers in borderline areas assume they are inside a city when they are not, or vice versa.

- If your home is in a city with a high transfer tax (Oakland, Berkeley, Albany, El Cerrito, Alameda), factor that cost into your net proceeds calculation from the outset. Do not leave it for the seller’s closing statement to deliver as a surprise.

- For Oakland sellers: identify your transfer tax tier (the applicable rate depends on the sale price), factor in the sidewalk and sewer lateral compliance requirements, and start the compliance process well before you list. POS compliance issues discovered mid-transaction delay closings.

- For Berkeley sellers: the BESO energy assessment is required. Get it done before listing so you have the report in hand for the disclosure package. The sewer lateral compliance requirement also applies.

- In unincorporated areas, disclose all special assessments (Mello-Roos CFD taxes, GHAD assessments, 1915 Bond Act assessments) accurately on the Natural Hazard Disclosure property tax addendum. These must be disclosed and are material to a buyer’s cost analysis.

- If your unincorporated property is on a private road, in an HOA, or served by a mutual water company or private utility, disclose those obligations fully. They affect carrying costs and may affect a buyer’s financing.

For Buyers

- Before making an offer on any property, ask your agent to identify the precise jurisdiction (city or unincorporated county) and the current transfer tax rate for that jurisdiction. In Alameda County particularly, this number can run to five figures and must be budgeted before the offer is written.

- Determine who pays the transfer tax by custom in that jurisdiction. In Alameda County, the county DTT is typically a buyer cost. Oakland’s city tax is a 50/50 split. Berkeley’s city tax is traditionally a buyer cost. Contra Costa County’s DTT is typically a seller cost. These customs can be negotiated, but you need to know the starting point.

- Request a complete Natural Hazard Disclosure report that includes the property tax addendum. Read the Mello-Roos and special assessment disclosures carefully. Ask how many years remain on any CFD bonds outstanding, and calculate the annual carrying cost.

- Look up the property’s Tax Rate Area (TRA) on the County Assessor’s website. Find the effective tax rate for that TRA and apply it to the purchase price to estimate your Year 1 tax bill. Do not use the seller’s current bill.

- For any property in a FHSZ or unincorporated hillside area, obtain homeowners insurance quotes from multiple carriers before removing your contingencies. The cost of insurance — or its unavailability at standard market rates — is a material factor in the total cost of ownership.

- If the property is in an HOA (common in unincorporated Alamo, Blackhawk, and similar master-planned communities), review the HOA’s financials, reserve fund status, and CC&Rs. Monthly HOA fees in Blackhawk, for example, can be $300 to $600 or more per month — a real carrying cost that a non-HOA city home does not impose.

- For properties in unincorporated areas served by a GHAD, review the district’s current assessment amount and its reserve fund. A GHAD with an underfunded reserve may levy a special assessment in future years for major slope remediation work.

CONCLUSION

The question “Is buying in an unincorporated area of Contra Costa or Alameda County cheaper?” does not have a single answer. It depends on which county, which community, and which city you are comparing it to. But the analysis is manageable once you understand the framework.

At the closing table, the single largest variable is the documentary transfer tax. In Contra Costa County, most cities impose no city transfer tax, so the comparison between unincorporated communities and most CCC cities is essentially equal. The important exceptions are Richmond and El Cerrito, where unincorporated addresses carry a significant closing cost advantage. In Alameda County, the gap is dramatic: unincorporated areas pay only the county’s $1.10/$1,000 while Oakland, Berkeley, Albany, Alameda, Emeryville, Piedmont, and San Leandro all impose substantial city-level taxes. On a $1.5 million sale, the transfer tax difference between unincorporated Castro Valley and Berkeley can exceed $22,000.

On an annual ownership basis, the comparison is more nuanced. Effective property tax rates are driven by the cumulative weight of school district bonds, city bonds, parcel taxes, Mello-Roos CFD taxes, GHAD assessments, and other special charges — not simply by whether a property is inside or outside a city. Unincorporated areas are not automatically lower-tax environments. However, they generally avoid the densest layers of city-specific parcel taxes that characterize Berkeley and Oakland tax bills, and they carry no city point-of-sale compliance obligations at the time of sale.

The factors that can cut against an unincorporated address: GHAD assessments in hillside communities, fire insurance cost and availability in FHSZ-designated areas, HOA fees in master-planned communities, and Mello-Roos taxes in newer subdivisions. Any one of these can narrow or eliminate the financial advantage that the absence of a city transfer tax creates.

Finally, beyond the purely financial: buying in an unincorporated area means your government is the county Board of Supervisors, not a city council. Your law enforcement is the county sheriff, not a city police department. Your planning and code enforcement are administered by the county. Whether that is preferable or not depends on your situation and priorities — but it is a structural difference with real implications, and every informed buyer and seller should understand it before signing.

DISCLAIMER: This article is intended for general informational purposes only and does not constitute legal or tax advice specific to any reader’s situation. Transfer tax ordinances, special assessment structures, point-of-sale requirements, and tax rates are subject to change. All rates should be independently verified with the applicable county recorder, city finance department, or escrow company before closing. The author is licensed as a California real estate broker and attorney. Nothing in this article creates an attorney-client relationship. Readers are encouraged to consult a licensed California real estate attorney and a qualified tax advisor for guidance specific to their transaction.